Spending Smart Building to Smart City

Emmanuel François

Because the Smart Building is connected, it is turning into a platform for multiple services that help to enhance its value. Through its development, the Smart City is extending the continuum of services provided for the user (consum'actor) to the level of the territory. This mutation, based on the sharing economy, leads to the creation of new trades around these services. While energy, mobility and health care constitute the driving force, data is the key element, and its governance has become a topic of major importance. Who will ensure that data is governed with complete confidentiality and security? The stakes are whetting numerous investor appetites and may offer an opportunity for local governments.

If we consider buildings a third skin, it is because we generally spend more than 75% of our time in one. Just as almost all of us are connected today, so too are buildings. The vector of this connectivity is the Internet, which is de facto becoming the fourth fluid, on a par with water, gas or electricity. It is thereby impacted by the laws governing digital technology, and hence subject to shorter cycles in context of pooling and sharing. This does not mean we have to change buildings every three years the way we change telephones. Rather, buildings must be designed or upgraded with systems and infrastructures capable of adapting to this evolution at lower cost or they will become obsolete. This major shift is the focal point of the Smart Building Alliance for Smart Cities (SBA) through its Ready2Services baseline reference, which breaks the "smart" building concept into three distinct, separable layers – equipment with sensors and actuators, IP communication infrastructure and cloud applications – which must all be based on open standards and interoperable. This is absolutely necessary for a so-called “intelligent” building to become truly Smart, in other words, a genuine platform of services that directly affect its value. Thus, like the automotive industry, which now talks in terms of mobility and mobility-related services, the building industry must replace its old model and instead offer services related to multi-faceted, multi-purpose spaces. With digital technology, we are moving from the era of ownership to the era of use. This rapid, fundamental mutation, driven partly by generations that grew up in the digital age, is going to have profound effects on our society.

The (R)evolution now under way accelerated in 2016 as a result of several converging factors. First of all, users are asking for it. Their environment is increasingly connected, starting with their cars, and soon it will be hard to understand why buildings should be cut off from any form of connectivity and adaptive intelligence. There are tell-tale signs like the “HOME” screen icon in the new iPhone IOS, which can only increase public awareness. Then there is a major financial stake that is going to encourage the mutation. Indeed, Smart buildings are far more efficient and their efficiency directly impacts their valuation. Property management companies clearly understand they will need to renovate their property portfolios within the next 3-5 years or run the risk of significant devaluation. By relying on a Ready2Service infrastructure that pools several services such as energy management, maintenance & operation, space management, building management and general services, heath care and well-being, and tenant services, building shifts from being a cost center to a profit center, which is the prerequisite for undertaking the massive upgrading of all the buildings in France without the need for subsidies or other financial incentives.

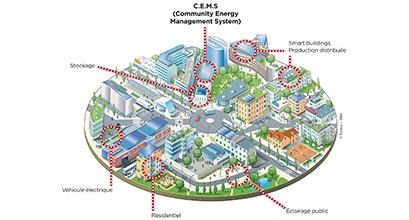

Naturally, for the user, this SMART environment should not be limited to buildings. It must extend to the region by providing service continuity to users through interoperability and open systems standards. Like the buildings, the region itself must be Ready2Services. This is indispensable to ensure the permanence of the systems and solutions introduced and gain the confidence of both investors and users. In this context, energy with the Smart Grid is the link between the Smart Building and the Smart City. With the development of electric cars and the need to reduce our CO² emissions, it is becoming urgent to think in terms of “Autonomous Buildings and Regions,” implying decentralized, low-carbon energy and maintaining a constant balance among the various networks. To achieve this, it will be necessary to have real-time information, for example concerning the energy consumption of building B at a given moment T, its tendency to decline, its ability to produce energy locally, store it and make it available and in what amount, at what point and over how long a period of time, etc. This represents a considerable mass of data that only complex algorithms based on artificial intelligence will be able to process insofar as they are accessible and available in a standardized format.

The SBA is working on this prerequisite through its Ready2Grid frame of reference. It aims to ensure that all new buildings constructed today or requiring upgrading will be Ready2Grid, just as they are or will be Ready2Services to be perfectly integrated in the SmartGrid and the SmartCity. The technologies, like those for the Smart Building, are ready and the models have been tested. The resulting efficiency more than justifies the investments and moving from the POOC (Proof of Concept) phase to wide-scale rollout insofar as the systems set up meet the open standards and interoperability criteria described in the Ready2Services and Ready2Grid baseline references. In today’s rather sluggish economic context, the Smart Building and Smart City definitely represent one of the best opportunities for the coming years available to all investors, whether private or public.

Of course that will mean challenging current business models by adopting a services approach in which the user becomes at once producer and consumer. As new modes of financing and transaction such as third party financing or the Blockchain emerge, it is essential to have legislative support for this transition. Indeed alternative models are now appearing, founded on participatory economics, which use digital technology to enable the pooling of equipment and systems to achieve high volume. These alternative approaches to traditional financing models, which are unquestionably far more flexible, could facilitate the transition to the Smart Building and the Smart City. They affect energy as well as all the services relating to the Smart Building and the Smart City.

In the process, many trades will have to evolve to support and guarantee the numerous services offered by “service operators” in Smart Buildings and Smart Cities. Major players from sectors such as energy, telecoms, IT, automation, facilities management and even real estate development are trying to position themselves in these new trades. In the era of digital technology and hence of globalization, other new players from the mobility, healthcare and insurance sectors are also likely to become legitimate competitors. In every case, inasmuch as local service is indispensable, data management will clearly be the common denominator. The ability to process multiple data is effectively a major criterion. Collecting, storing and processing data becomes an essential function of the Smart Building and the Smart City. That includes of course security and confidentiality, both key conditions to ensure user trust and therefore a prerequisite to higher volumes. An opportunity is opening up for local governments or, on a smaller scale, for common interest development associations (Associations Syndicales Libres, ASL) to present themselves to their constituents as trusted third parties capable of ensuring data management and many of the services related to it. In the long run, this evolution implies a new organization of the territory to make it more decentralized and locally accessible. The inevitable changes in work, stemming from digital technology, in the direction of greater flexibility through distance work or independent worker status are expected to support this trend thanks to the emergence of co-working centers that are likely to evolve towards multi-service third party places including, among others, a concierge service, the point of convergence of numerous services relating to a building or a neighborhood.

In general, with the help of digital technology, our society can now develop into an increasingly decentralized network organization, in which the individual assumes a central role as both consumer and actor. Informed in real time about their environment and the consequences of their acts, individuals cease to be “assisted” citizens and become “responsible” or “co-responsible” citizens. They take the time to reach out to others through third places where they can renew social ties with friends and neighbors while enjoying wider access to community services.

This mutation of our society must materialize at the level of the Smart Building and from there extend to the Smart City. Energy, mobility and health care are undeniably the main forces driving the transition to achieve greater efficiency, well-being and improved social cohesion.

Emmanuel FRANCOIS

President of the Smart Buildings Alliance for Smart Cities